OTAs vs. Supplier-direct bookings in Eastern Europe

- Published:

- August 2021

- Analyst:

- Phocuswright Research

Like the rest of the world, the Eastern Europe region has not escaped the COVID-19 pandemic, although each country's government response has differed, according to Phocuswright's latest travel research report Eastern Europe Travel Market Report 2020-2024. Bulgaria was among the hardest hit by COVID, and still required proof of vaccination, recovery from COVID or a negative COVID test to enter the country as of July 2021. Conversely, in Greece, where 20% of the population is employed in the tourism sector, most travel restrictions were lifted in spring 2021 and inbound visitors from 53 approved countries could enter the country without having to quarantine. Russia eased many of its COVID-related restrictions in May 2020, and its residents were quick to book domestic trips, such as to Sochi's beaches or cultural excursions in Moscow and St. Petersburg.

Domestic travel has, in fact, been a lifeline for several Eastern Europe travel markets, where COVID vaccination rates remain stubbornly low. In Russia, Bulgaria and Ukraine, for example, less than 20% of each country's population had been fully vaccinated against COVID-19 by early August 2021. With a history of living behind the Soviet Union's "Iron Curtain," many Eastern Europeans have a strong desire to travel despite the risks. Residents of the region's densely populated capitals, including Moscow, Prague, Budapest and Warsaw, have used frequent weekend getaways to scenic forests, beaches and mountains to satisfy their wanderlust.

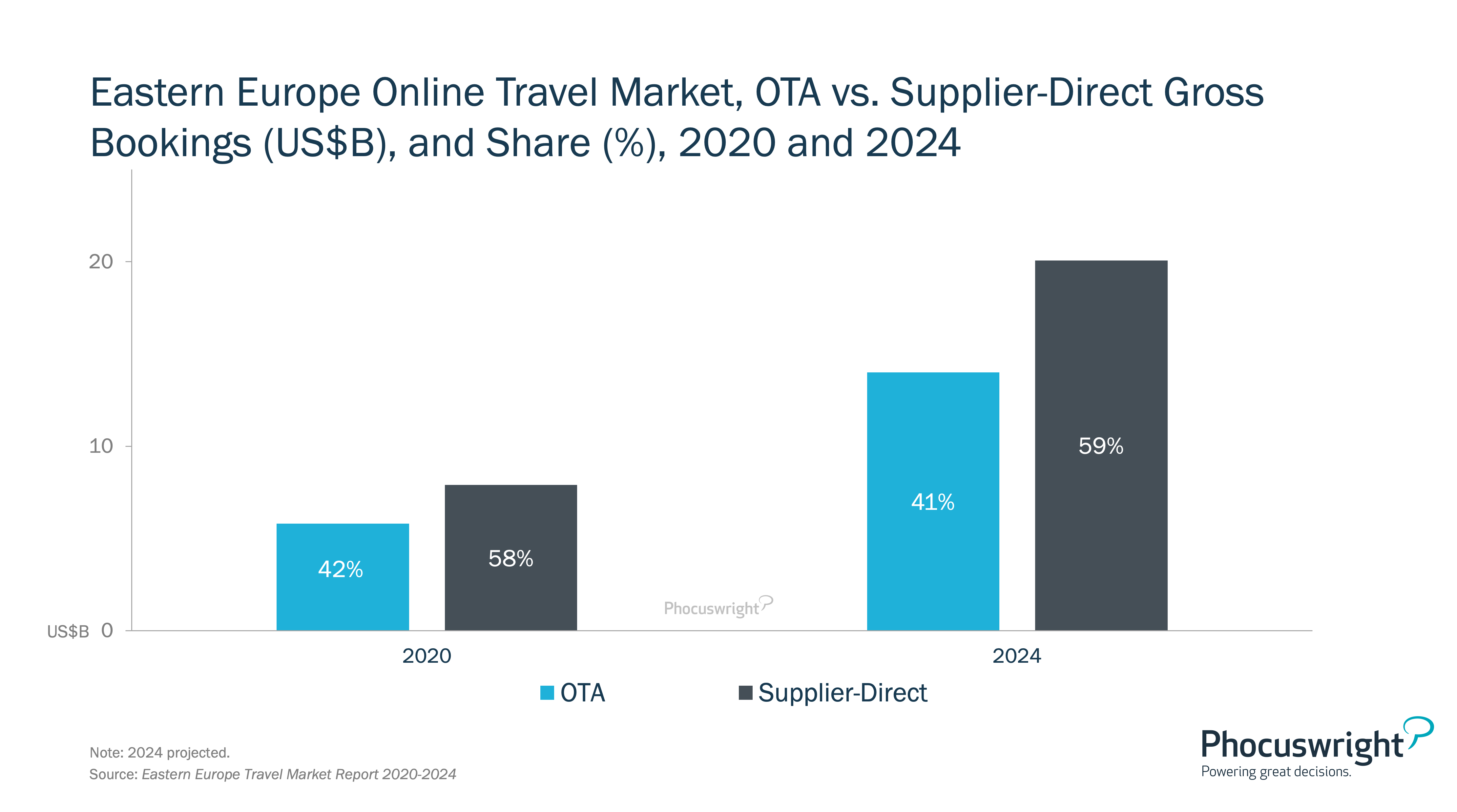

OTAs vs. Supplier-direct

In Eastern Europe, travel market distribution will shift online over the next four years, prompted by near-universal internet access and smartphone use. Though Eastern Europeans generally prefer to book trips through traditional channels, pandemic restrictions forced many people to research and purchase online.

OTAs will lose ground to travel suppliers, which will combine pandemic-based government subsidies with technology investments to improve the ease-of-use and functionality of their websites and mobile apps. As a result, supplier share of the online travel market will expand from 58% in 2020 to a projected 59% in 2024 (see figure below). OTAs will maintain an edge in Eastern Europe's fragmented hotel market, but struggle to keep up with government-backed suppliers in the airline and rail segments.

(Click image to view a larger version.)

While case counts fluctuate in mid-2021 and vaccine hesitancy persists, regional and domestic travel are the main lifeline for the industry. Recovery is taking foot, but unrolling slowly. In most segments, online penetration is rising, with particularly high mobile search use. The full report Eastern Europe Travel Market Report 2020-2024 provides market sizing, projections and key segment analysis for the Eastern Europe travel industry through 2024, including Bulgaria, Czechia (a.k.a. Czech Republic), Estonia, Hungary, Greece, Latvia, Lithuania, Poland, Romania, Russia and Ukraine.

If you become a Phocuswright Open Access subscriber, this report and the entire Phocuswright research library (and interactive data visualization tools) are available to you and your company. Phocuswright works closely with companies in all sectors of the travel industry to provide the research and data needed to make smart business decisions. Explore the Open Access benefits best suited to your company.

More Research Insights