U.S. hotel and lodging 2026: Slow growth, a stable split and AI waiting at the door

- Published:

- June 2026

- Analyst:

- Phocuswright Research

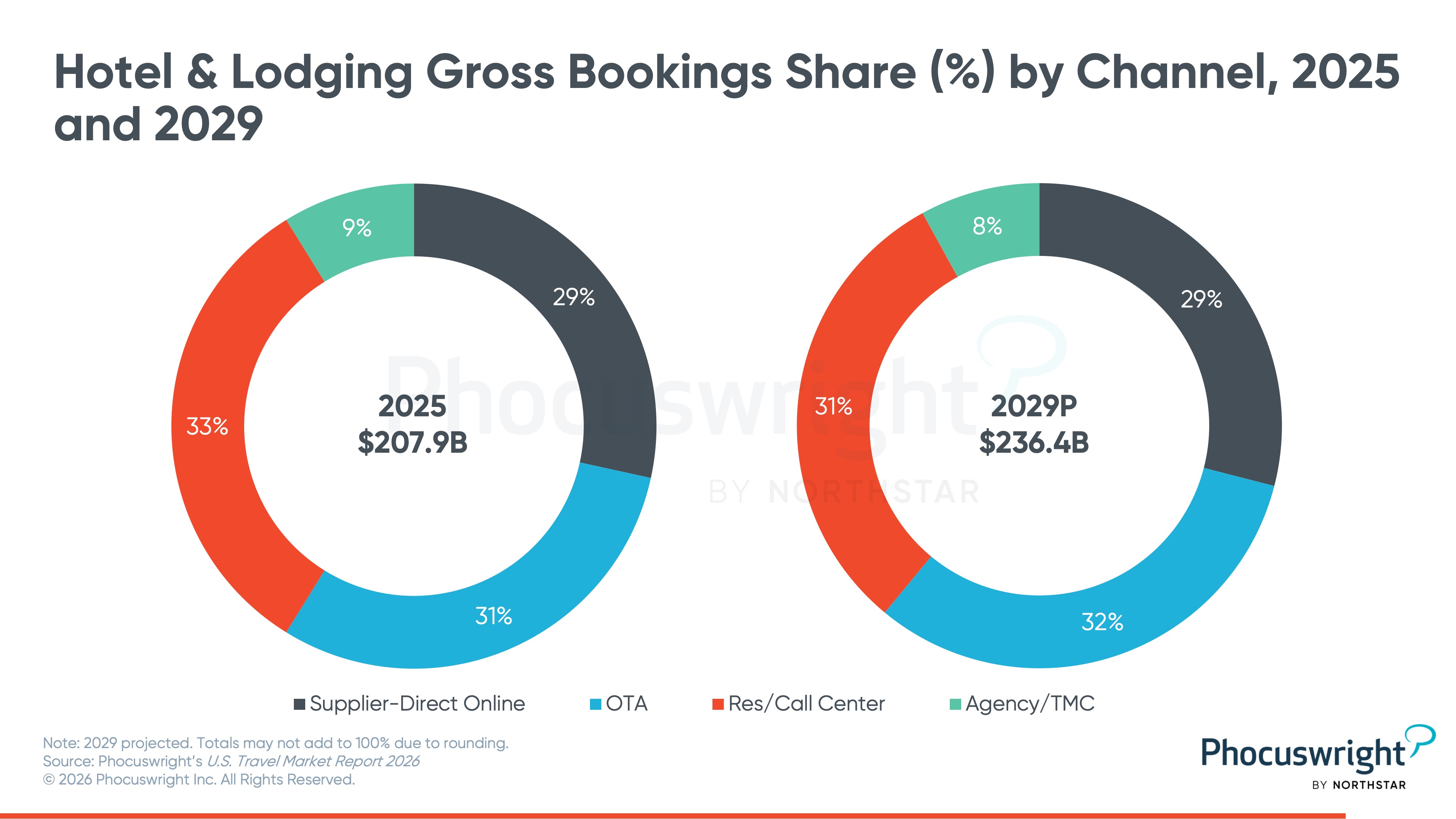

The U.S. hotel market is navigating a period of measured growth and competing pressures. According to Phocuswright's report U.S. Hotel & Lodging Travel Market Essentials 2026, room revenue rose 1% to $207.9 billion in 2025, with average daily rates (ADR) up just 1% and occupancy falling to 62.3% — the first decline since 2020. The number of rooms sold was essentially flat. These are not crisis-level figures, but they signal a market running low on the tailwinds that powered post-pandemic recovery.

The outlook for 2026 is cautiously better. Room revenue is projected to gain 3% to $214.7 billion, supported by modest ADR improvement and higher demand. But the path carries real risk. The continued lag in international arrivals, driven by stricter travel policies, geopolitical tension and anti-American sentiment, remains a meaningful drag. Weakness in key source markets, including Canada, compounds the issue. Offsetting that: strength in luxury and a rebound in corporate travel and large events should absorb some of the shortfall. High-profile demand catalysts like the FIFA World Cup and America 250 add potential upside, though how they translate to actual bookings remains unclear.

Hotels now account for 41% of U.S. travel gross bookings, just behind airlines at 42%. The fastest-growing segment is online, up 4% in 2025 against a flat offline channel. Within online, the split between online travel agencies (OTAs) and hotel websites and apps sits at 52%/48% respectively and is expected to hold steady through 2029. OTAs are gaining momentum, led by B2B offerings and technology investment, and are projected to outpace every other channel in 2026 and 2027. Branded hotels are pushing back through loyalty, adding millions of new members and shifting volume away from the offline channel. The net result is a distribution landscape that looks stable on the surface but is actively being contested underneath.

AI: Marketing Tool Today, Distribution Channel Tomorrow

Artificial intelligence is a top priority across hotel operations, with marketing, customer service, revenue management and operations all in active transformation. The near-term focus is concrete: deploying chatbots to handle guest queries and personalized recommendations, and generating content optimized for visibility on AI-powered search platforms. Hotels with strong brand equity, loyal customer bases and proprietary content are best positioned to benefit from these shifts as AI becomes a more central part of how travelers plan and book trips.

The longer-term distribution implications are less settled. AI platforms are currently operating at the top of the funnel, functioning largely as a replacement for traditional search rather than a booking mechanism. OTAs and metasearch engines have already moved to establish a presence: Expedia and Kayak, for example, have booking plug-ins integrated into ChatGPT. But if AI-first platforms such as ChatGPT, Google Gemini and Anthropic Claude expand into direct booking, they could emerge as a new distribution channel entirely. How that reshapes the competitive balance between OTAs, branded direct and AI-native platforms is one of the more consequential open questions facing the industry.

More Research Insights