A market rewired: Ten structural shifts redefining Asia Pacific travel

- Published:

- July 2026

- Analyst:

- Phocuswright Research

Asia Pacific travel is no longer moving in a single direction. Ten structural shifts, spanning demographics, geopolitics, infrastructure, capital and technology, are reshaping demand, and Phocuswright's newest report argues they're interacting rather than acting alone.

The demographic divide is widening. India, Indonesia and Malaysia remain young and urbanizing, with large cohorts entering peak travel years. Japan, South Korea and Taiwan sit at the opposite extreme: Japan already has nearly 30% of its population over 65, and South Korea and Taiwan post some of the world's lowest fertility rates. China, Thailand, Australia and New Zealand occupy the middle, with slowing growth but strong current spending power.

Geopolitics is moving demand in real time. Cambodia's foreign arrivals fell more than 36% year-over-year amid border tensions with Thailand. Escalating diplomatic friction with China contributed to a forecast 3% drop in Japan's 2026 inbound visitors, worth up to ¥1.2 trillion ($7.7 billion) in lost spending. Meanwhile, the India-China air corridor reopened in late 2025 after a five-year suspension, and interest in travel between the two countries surged roughly 1,800% year-over-year.

Travel maps are reordering. Thailand (-7%) and Cambodia (-4%) lost ground in 2025 while Vietnam, Japan, Indonesia and Central Asia gained share through visa liberalization, capacity growth and deliberate destination repositioning.

Rail is becoming a geography-shaping force, not just a mode of transport. Its share of APAC gross bookings is projected to grow from 21% in 2025 to 22% by 2028, powered by new cross-border links, sleeper services and a younger generation favoring slower, immersive trips over packed itineraries.

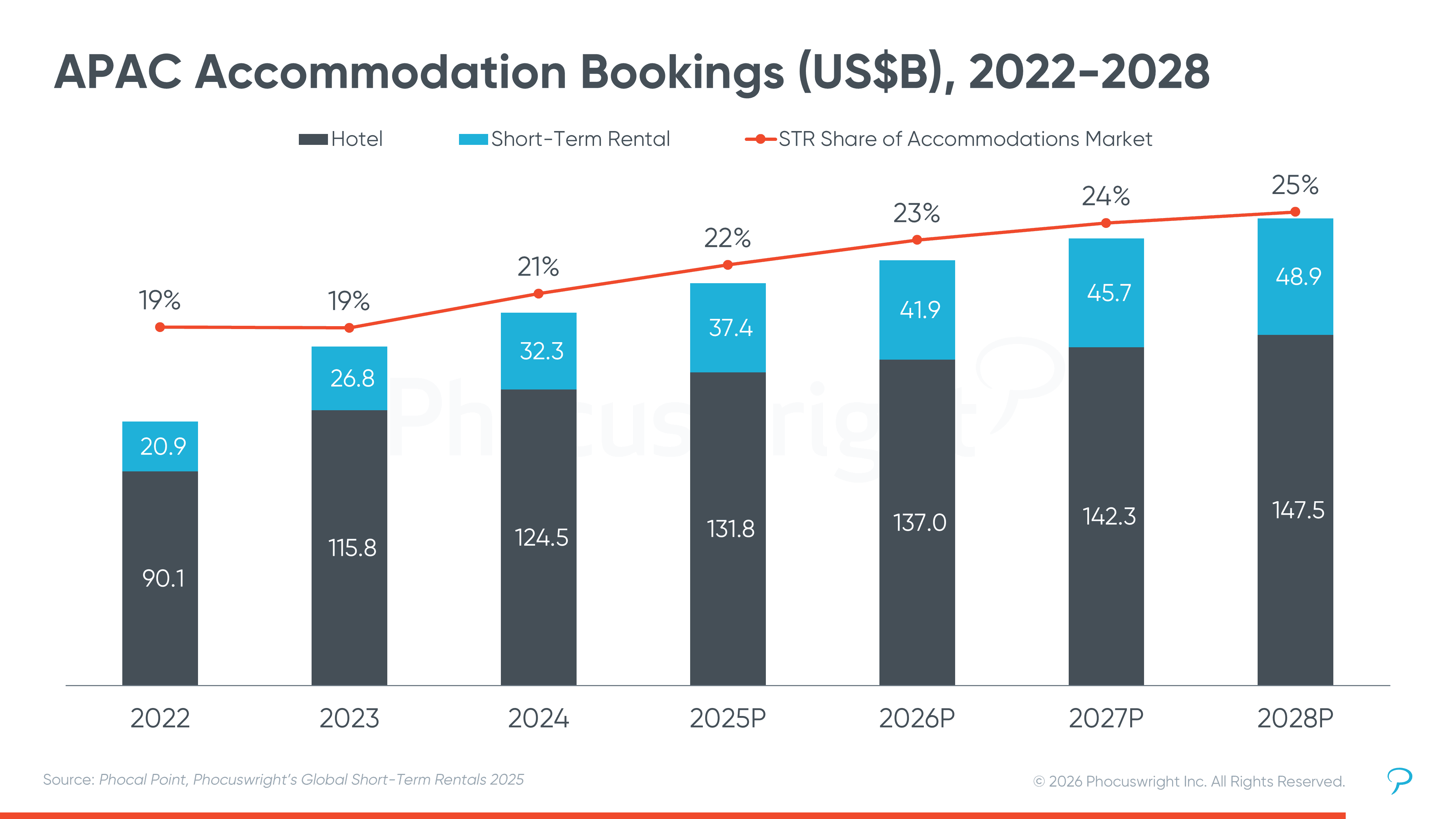

Short-term rentals have become structural, not cyclical. Their share of the APAC accommodation market is set to rise from 22% in 2025 to 25% by 2028, worth $48.9 billion, driven by dense cities like Shanghai, Tokyo and Seoul where hotel supply can't scale fast enough.

Fintech has become travel infrastructure. APAC accounts for nearly half the global fintech market, with transaction volumes projected at $19 trillion in 2025. BNPL is now embedded across bookings on platforms like MakeMyTrip and Traveloka, while China's super apps have normalized instant refunds and wallet-based rebooking as consumer expectations.

Hotel globalization is flowing outbound. Chinese groups Jin Jiang and H World, India's IHCL and OYO, and Korea's Lotte and Hotel Shilla are expanding abroad to follow their own outbound travelers, treating international growth as loyalty retention rather than pure footprint expansion.

Venture capital has tightened sharply. APAC travel startup funding hit its lowest level in five years in 2025. OYO turned profitable, Traveloka reached positive EBITDA, and Klook is eyeing a U.S. IPO, all rewarding operational discipline over expansion-at-all-costs.

Cross-industry partnerships are the new distribution channel. Marriott Bonvoy now earns points through Flipkart purchases in India. Alipay+ Voyager embeds full trip booking inside China's super apps. Grab bundles travel services like eSIMs into its ride-hailing app. Travel brands are competing on where they show up in daily digital life, not just on inventory or price.

The report's conclusion: advantage will go to companies that adapt across all of these forces at once, not to those chasing volume in any single one.

Phocuswright powers the travel industry’s smartest decisions. Make confident, data-driven decisions that outpace your competition by leveraging our in-depth insights and analysis.

The Phocuswright Open Access research subscription gives you company-wide access to all of our expert-driven research reports and interactive data, so your team can identify emerging trends and seize new opportunities faster. Learn how it works.

More Research Insights