Strong consumer spending meets economic crosscurrents — and the outcome matters for travel.

An excerpt from Phocuswright's U.S. Travel Market Report 2025

The U.S. economy demonstrated resilience in 2024, growing by an estimated 2.8%, despite weathering persistent challenges such as elevated interest rates, lingering inflationary pressures and global geopolitical uncertainties. Consumer spending, a primary driver of economic growth, remained strong, supported by wage increases and enduring demand for experience-based consumption. However, signs of strain emerged in the employment landscape as the year progressed. After holding below 4% for over two years, the national unemployment rate rose to 4% in May 2024 and remained above that level through the first half of 2025. This shift was driven by widespread layoffs in the technology sector—including at Amazon, Meta and Google—as well as job cuts across retail (Walmart, Target) and financial services (JPMorgan Chase, Citigroup). The rise in unemployment introduces downside risk for discretionary categories such as travel, particularly among middle-income households more exposed to job market volatility.

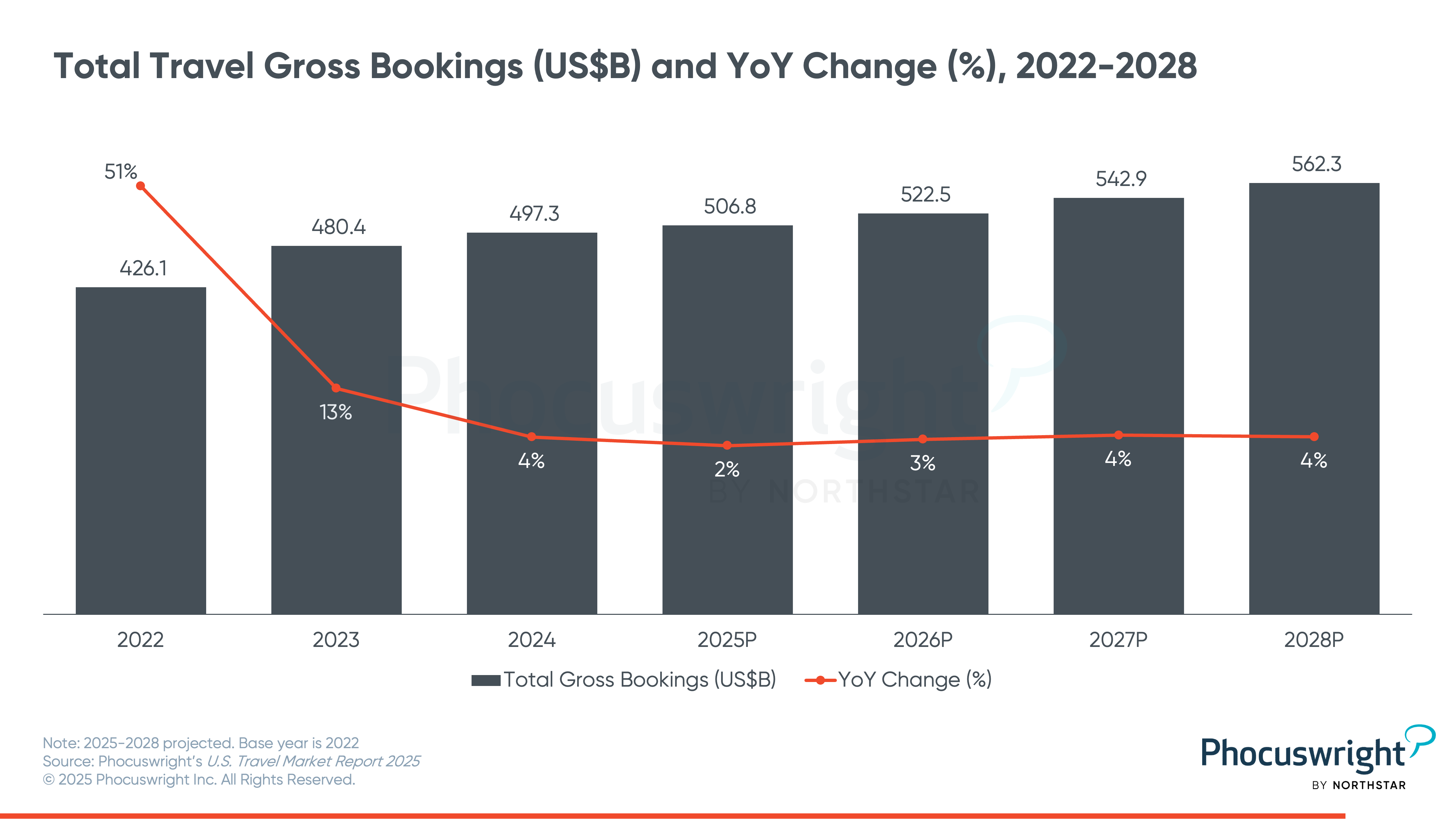

The U.S. travel industry expanded by 4% in 2024, reaching a total market value of $497.3 billion. While demand remained healthy, the pace of growth moderated as the industry transitioned out of the post-pandemic surge period. Travel suppliers, which had previously benefited from elevated pricing power amid strong pent-up demand, began to face mounting pressure on rates as consumer sensitivity to cost returned and competitive dynamics intensified. Nevertheless, domestic travel remained a key growth engine, buoyed by sustained leisure demand and a gradual rebound in corporate travel activity.

After growing by 9% in 2024 (to 72.4 million), U.S. inbound travel appeared to be on a recovery path.

Outbound travel from the U.S. sustained robust activity in 2024, with total departures exceeding 107 million and surpassing pre-pandemic peaks, according to the U.S. Department of Commerce. A strong U.S. dollar and a continued appetite for international experiences helped fuel the surge, supported by smoother passport processing and stable airline capacity. Early 2025 data shows a modest deceleration, driven by geopolitical tensions and tighter immigration policies in some markets—though outbound travel is still growing year over year. That said, this growth primarily benefits airlines and, to a lesser extent, packaged tour providers as most in-destination spend occurs abroad, representing a lost opportunity for U.S.-based travel suppliers.

After growing by 9% in 2024 (to 72.4 million), U.S. inbound travel appeared to be on a recovery path, though it still fell short of pre-pandemic highs. While the upward trajectory held, challenges persisted: Visa wait times remained lengthy, and regional destinations increasingly drew travelers away from long-haul options—particularly in Asia Pacific. In the first half of 2025, the rebound had all but stalled, with arrivals declining from several key markets, including vital neighbors Canada and Mexico. The U.S. government's increasingly unwelcoming tone, including its stance toward specific nationalities and communities, stands in stark contrast to global trends, as other destinations aggressively court international tourists. In June, a sweeping travel ban affecting 19 countries added to the headwinds for inbound travel. While not the primary cause, actions like these contribute to a broader narrative that, per WTTC estimates, may cost the U.S. $12.5 billion in international visitor spending in 2025.

The U.S. travel industry is navigating a highly volatile policy landscape, with sweeping regulatory shifts impacting multiple sectors. Airlines and tour operators are dealing with stringent entry restrictions and intensified border scrutiny, driving up operational load. Hotels, short-term rentals and OTAs are adapting to new FTC transparency rules on fee disclosures, which may impact distribution and competitive dynamics. Persistent labor shortages across airlines, hotels and car rentals have exacerbated staffing expenses, complicating operations. Efforts to revive America's image among international travelers face hurdles, worsened by a planned 80% cut in Brand USA funding—from $100 million to just $20 million. Despite these challenges, ongoing investments in infrastructure, rapid adoption of generative AI to boost efficiency and personalization, and Americans' unwavering enthusiasm for travel promise continued resilience and growth.

This insight is just the beginning.

The excerpt you’ve read comes from Phocuswright’s U.S. Travel Market Report 2025, the definitive resource for executives navigating the shifting economic and competitive landscape. Inside, our analysts break down the full market sizing, growth projections, segment-by-segment performance, and the forces that will shape traveler behavior in the months and years ahead.

In a climate where GDP growth coexists with rising unemployment, and where consumer confidence can turn on a dime, the stakes have never been higher. Your competitors are already scanning the horizon for threats — and opportunities. Without this depth of data, you’re flying blind.

Don’t leave your future strategy to guesswork. Get the complete report today and arm your team with the intelligence needed to make confident, timely decisions that protect market share and drive growth.

See what insights you're missing

More Research Insights