The state of startup funding

- Published:

- August 2022

- Analyst:

- Phocuswright Research

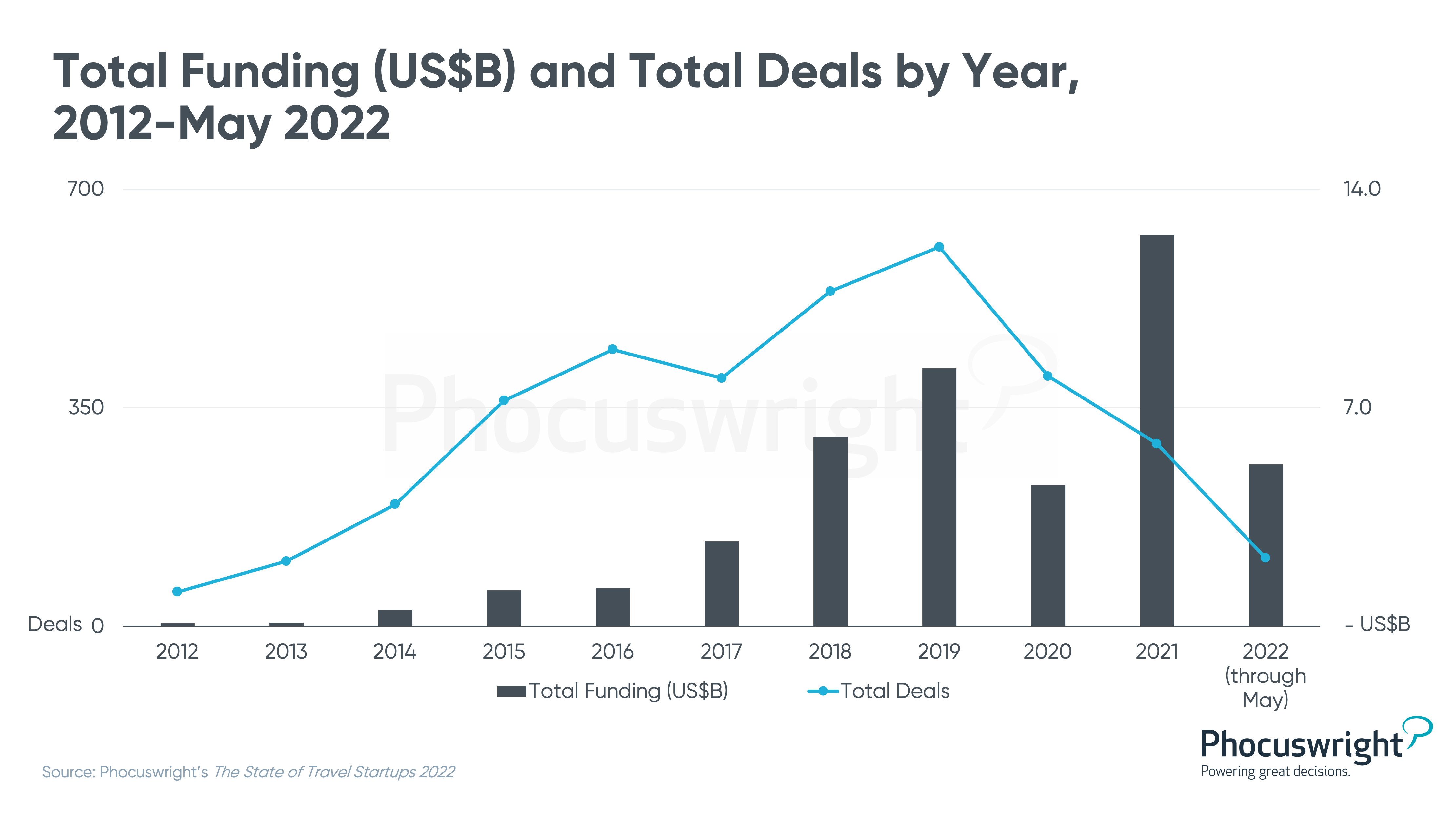

After crashing by 45% to just $4.5 billion in 2020, annual funding to travel startups recovered impressively in 2021, clocking in at $12.5 billion, far exceeding the previous high of $8.3 billion in 2019, according to Phocuswright’s latest travel research report The State of Travel Startups 2022.

This represents a significant comeback, leaving little doubt that investors "bought the dip" and are betting on a full recovery of the industry sooner rather than later. Furthermore, as of the second quarter of 2022, signs point to a continuation of funding activity in step with the travel industry at large.

(Click image to

view a larger version.)

Investments in travel startups through May stood at just over 40% of the total funding raised in all of 2021. If 2022 funding exceeds 2021, it would be all the more remarkable, given that the financial markets are tightening and inflation is ramping up.

Though travel was hit harder by the pandemic than most industries, it has followed a similar route to recovery. An early 2022 Crunchbase analysis found that across industries, 2021 shattered all records for both global venture funding and unicorn creation (companies worth $1 billion or more).

Most of this can be attributed to low interest rates, resulting in low cost of capital, which had a multipronged effect on both public and private markets. First, it sent public market valuations soaring. Then, as investors sought relatively "cheaper" deals, it pushed private valuations up as well. Crunchbase notes that "New unicorns joined our board at a dizzying pace, with 586 new entrants - averaging more than 10 new unicorn startups per week. For comparison, 2020 minted 167 new unicorn companies, averaging three per week."

Another explanation for the strong funding is that the pandemic increased urgency among organizations to make investing in technology-driven automation a top priority, something that had been sluggish in travel pre-pandemic and was overdue to catch up.

Although total dollars were up significantly, deal count slowed greatly. While both dollar amount and number of deals had peaked in 2019, far fewer funding rounds occurred in 2021, despite the funding explosion.

Sustaining a trend Phocuswright has highlighted for years, funding continues to move later stage with ever-bigger funding rounds going to the perceived "winners" or potential winners in their respective categories. Thus, mid- and late-stage companies are benefiting the most.

There’s a lot more funding analysis in the full report, including funding raised by funding type, average funding round deal sizes and share of funding stages. In addition, the report gives a full investor analysis, vertical analysis of all major travel segments, horizontal analysis, business focuses, regional analysis and more. This crucial business knowledge of the market gives investors and businesses a complete understanding of the financial ecosystem, investing trends and knowledge, new venture initiatives and more.

For further intelligence for you and your entire company, subscribe to Phocuswright Open Access. This subscription puts the entire Phocuswright research library and powerful data visualization tools at your fingertips. There’s a reason executives around the world trust and reference Phocuswright research and data on a daily basis. Explore for yourself why.

More Research Insights