Research Insights

The State of Travel Startups

The State of Travel Startups

- Published:

- August 2014

- Analyst:

- Douglas Quinby

At Phocuswright, we get a lot of briefings from travel startups. Over the years, we have seen many emerging companies, so we decided to dig into the numbers to see what we could learn about the state of startups in travel – where are entrepreneurs investing their creative capital, and where are investors placing their bets?

Travel Startups – Companies & Dollars

First, we set a few parameters: companies had to be founded between 2005 and 2013 and they had to be focused on travel and digital. And they had to be real. We had to see a real product or at least have some credible and verifiable backing. In other words, there had to be a little more than a couple of developers in a garage or a fancy pitch deck.

We ended up including almost 750 travel startups. Combined, those companies raised approximately US$4.8 billion over the eight-year period. That includes angel, venture and later-stage investments as well as strategic acquisitions. We excluded IPOs.

Has the market been pretty hot? Well, the majority of that funding happened in just the last three years – more than $3.3 billion. This was led by some bigger deals with companies like trivago, Airbnb, Lyft, Uber and China's Qunar, eHi Car Rental and Kuaidadi (it excludes the monster rounds raised by Airbnb and Uber in 2014).

You could argue that ride-sharing and taxi-hailing services such as Kuaidadi, Lyft and Uber are not so much in travel as they are in local transportation. If we exclude them, a majority of the total funding would still have occurred within the last three years.

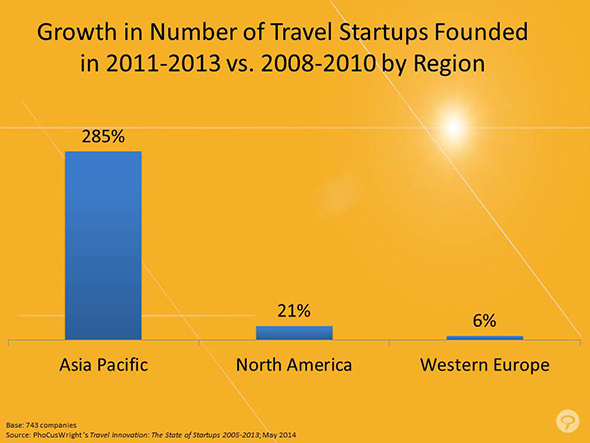

Asia's Spectacular Growth

One of the most exciting developments is the growth in startups coming from outside the U.S. and Europe. From 2011 to 2013, 30% of travel startups were founded in emerging market regions. Asia – led by China – is driving most of that growth.

Figure 1

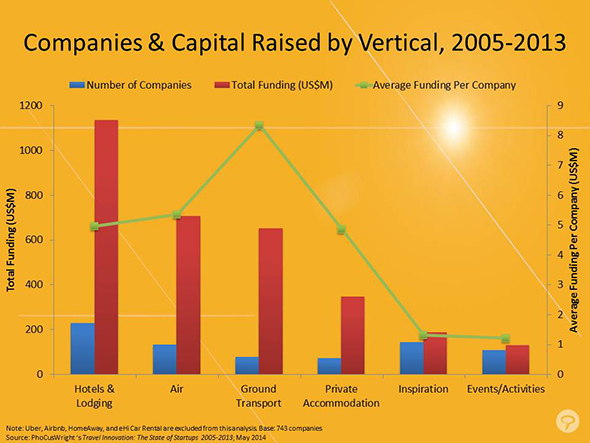

Startups by Travel Vertical

Travel really isn't an industry so much as an umbrella term housing a range of industries. This includes everything from big global airlines and hotel brands to online travel agencies, mom-and-pop tour operators, and the growing ranks of sharing economy participants listing homes on Airbnb and HomeAway, or offering local experiences through services like Vayable and EatWith. We sought to identify areas within travel that are generating the most significant interest from investors and entrepreneurs. So we undertook the painstaking task of manually reviewing and tagging each startup in two ways:

Vertical segment: the travel segment in which the startup operates (e.g., air, lodging, cruise, etc.).

Horizontal focus: the technology, medium or business area on which the company's activity is centered (e.g., search, booking, advertising, peer-to-peer, etc.).

Not surprisingly, lodging rules (see Figure 2 below). Lodging is the largest global travel industry segment (if you include all forms of lodging), and its relatively large margins drive the majority of industry profits for online agencies and other intermediaries. The 243 lodging-focused travel startups established between 2005 and 2013 collectively raised nearly $1.2 billion.

Figure 2

But more telling than the total funding or number of companies is the average funding per company (the green line in Figure 2, which correlates to the secondary Y axis on the right). This gives an indication of where both entrepreneurs and investors see the biggest opportunities, or where there might be a mismatch. Ground transportation – which includes the many ride-sharing and taxi hailing apps as well as startups focused on car rental, bus and rail – has the highest funding per company. (Note: we have excluded a handful of companies, such as Airbnb, eHi Car Rental, HomeAway and Uber, whose total funding has been so large that it would skew the category averages.)

One interesting vertical category is "inspiration," second from the right in Figure 2. We created this for the many travel startups focused not so much on a single traditional vertical, such as flights or hotels, but rather on the broader activity of trip planning, discovery and inspiration. This includes social travel startups, trip organizers, mobile content guides and other services. This category may be the second largest after lodging (nearly 200 companies), but it has one of the lowest per-company funding averages. While a lot of entrepreneurs see opportunity in the inspiration and travel planning phase of travel, investors aren't buying in.

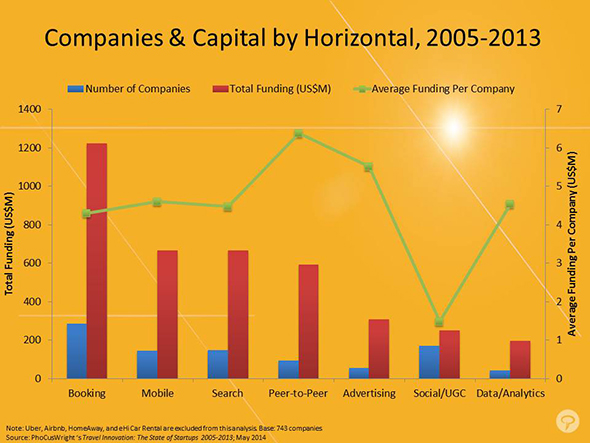

Startups by Horizontal

We also analyzed startups by their commercial or technical area of focus. In other words, is their horizontal focus transactional (bookings), mobile, social media, advertising, etc. There is definitely some overlap here, as well as some subjectivity to the categorization. (For example, what defines a "mobile" travel startup, when virtually every travel company today must have a mobile play.) So we took pains to designate companies to a horizontal according to their core strategic focus. For example, Airbnb has a great mobile experience, but mobile is not their mission; it's creating a peer-to-peer marketplace for lodging (and likely other related services in the future). So we tagged Airbnb as peer-to-peer, not mobile. HotelTonight is about mobile-only last-minute hotel bookings (you can only book a "HotelTonight" on mobile). So they are tagged for mobile.

The biggest horizontal category is, not surprisingly, booking (see Figure 3 below). The transaction is where the revenue is, and many of these startups are companies bringing online transactional services into new markets. Those could be new geographies, such as Latin America or Russia, or new verticals, such as vacation rentals or local events and activities, where there have been limited online booking and payment options for travelers.

Figure 3

Again the green line (average funding per company in each horizontal) is telling. The largest sectors on a per capita funding basis are peer-to-peer, advertising and data and analytics. Social/UGC is the second largest focus area for travel startups – a lot of entrepreneurs are trying to create the next TripAdvisor or Facebook for travel – but investors seem to have decided there already is a Facebook for travel (it's called Facebook).

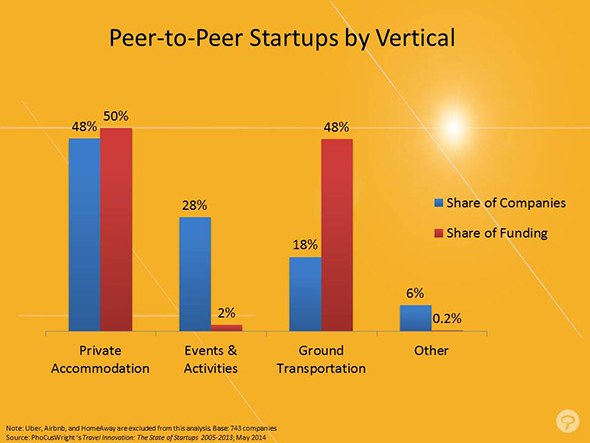

Travel's Sharing Economy Startups

The sharing economy is definitely having its day in the sun. Among the more than 90 peer-to-peer companies, there are two dominant vertical categories: lodging and ground transportation. The lodging peer-to-peer category includes Airbnb, HomeAway and their myriad imitators, while ground transportation includes the well-known ride-sharing services, as well as car rental plays such as FlightCar and RelayRides.

A third interesting category is in-destination tours and activities, where startups such as Vayable and Withlocals are creating marketplaces for local residents to become local guides. While this latter category is home to a number of startups, it accounts for just a sliver of travel's peer-to-peer funding pie.

Figure 4

Slam-Dunks or a Long Struggle?

The big question for these nearly 750 startups is, how many have been successful? Of course, that depends on the definition of success. There have certainly been a few eye-popping exits, such as HomeAway, KAYAK, Qunar, trivago and Tuniu. There have been some incredible rounds of funding, including Airbnb, HomeAway, Uber, Lyft, eHi, Kuaidadi and Wimdu.

But when it comes to acquisitions, the numbers are pretty small. Fewer than one in 10 companies have been acquired. And many of those acquisitions were not the big exits their founders (and investors) likely hoped for, but distressed asset sales or acqui-hires for developer talent.

However, the good news is that only one in five of those companies has closed. The majority are still either working toward that next round, profitability, or even that dreamed-of acquisition or IPO.

More Travel Startups?

Phocuswright's Travel Innovation: The State of Startups 2005-2013 features much more analysis and detailed information on the roughly 750 companies we explored.

More Research Insights

Beyond points: Rethinking loyalty and brand consistency

Hope isn't lost in the endeavor to increase brand consistency, but travel companies may need to...

Read More

The supplier shift powering Latin America’s travel growth

Latin America’s travel industry proved remarkably resilient in 2024, generating US$67.9 billion in...

Read More

From $1.6T to $1.8T: How global travel will grow, shift and digitize by 2027

Forces point to steady but uneven expansion, with global gross bookings projected to grow an average...

Read More

When travel isn’t first: How economic strains are changing consumer behavior

While travel incidence held steady in 2025, spending has tightened as Americans weigh travel against...

Read More

Momentum and bottlenecks: India’s aviation in focus

India’s travel market is accelerating at a pace few global sectors can match. Gross bookings climbed...

Read More

The five developments driving the evolution of U.S. OTAs

Amid cooling domestic demand, U.S. online travel agencies are adapting to a more competitive and...

Read More

7 powerful shifts driving the Middle East’s travel boom

The Middle East has emerged as one of the fastest-growing travel markets globally, supported by...

Read More

$407B by 2028? The numbers behind U.S. corporate travel’s new trajectory

Business travel is entering a new era, shaped by the convergence of technological innovation, shifting...

Read More

Growth without lift in China’s $151.8B travel market

China’s travel market is full of contradictions. Demand is surging, yet deflation and shaky consumer...

Read More

ANZ travel market outlook: Growth fueled by prices, not passengers

The ANZ travel market offers opportunity, but not without challenges. Growth is real, but it is being...

Read More