No Travel Experience Necessary: More Outsiders Enter the OTA Market

This article is part of a content series that explores some of the most impactful innovation and technology-driven trends that will influence the travel industry in 2023 and beyond.

Non-travel brands, such as financial institutions, retailers and loyalty clubs, must really want to get into the travel business. Over the past two years, several have launched travel booking platforms or announced ambitious plans to do so, even though the online travel agency market is already near saturation and uber competitive. Will they succeed? If so, what are their advantages and what will be the impact on the marketplace?

It's the 1980s, and the travel industry is about to get shell shocked. Online services like Prodigy, CompuServe and America Online have just put incredible power into the hands of consumers, including access to real-time sports, weather, news and travel advice. E-commerce soon follows, and online travel planning and booking becomes routine. New business opportunities emerge. Travel retailing is no longer solely in the hands of trained agents who’ve mastered the GDS “green screen.” Now anyone with a plan can create a travel storefront by plugging into airline, hotel or other travel inventory. Entrepreneurs flock to travel like moths to a lightbulb, and the online travel agency (OTA) is born.

Following two decades of consolidation, two main players have come to dominate the OTA space: Expedia Inc. and Booking Holdings. Millions of consumers access their various brands for low prices and breadth of content. There are also myriad local, regional and specialized players competing for their share of travel spend, including Trip.com, Hopper and eDreams. Considering the already crowded landscape, there would appear to be little room for new travel brands to emerge, especially those that don’t have roots or deep knowledge in the industry. Any new OTA is often met with skepticism, but that hasn’t stopped a slew of new hopefuls from other sectors such as banking, retail and membership organizations from taking a shot. Can they compete with the big brands? Do they even need to?

Ironically, it’s the existing players – Expedia, Booking and Hopper – that have the most to gain from this trend. Plug-and-play options offered by Expedia for Business, Rocket Travel (Booking.com) and Hopper Cloud make it easy for institutions and organizations to provide private-label travel offerings with little or no expertise. There’s limited work to do, since in most cases partners don’t have to settle the transaction, fulfill the product or even provide customer service.

Most OTAs’ private-label partners are travel suppliers such as airlines and agencies looking to supplement inventory and revenue. But the others represent the long tail, including non-travel brands such as banks, retailers, rewards programs and membership-based organizations seeking to add value to their current offerings and further monetize their existing audiences. Most of these non-travel companies don’t expect to compete with the giants, or even to make a lot of money. Rather, their goal is to provide a convenient service to customers, so they keep coming back. And though their travel gross bookings are tiny compared to the big OTAs, the benefits can be big in terms of generating customer loyalty and, for financial institutions, usage of their card(s).

We Are All Travel Brands

Chances are, even if you’re not a travel business, your customer likes to stay in hotels or take vacations. Travel is so universal and desirable, that imbedding it into other products and services has a good chance of attracting eyeballs and enhancing a business’s main offerings. One of Expedia’s best-known, private-label partners isn’t from travel at all, but is rather a non-profit that advocates for seniors. Washington, DC-based AARP offers special discounts to its 38 million members via the AARP Travel Center Powered by Expedia (see Figure 1). AARP has had time to build a following, having launched its travel site with Travelocity in 2004 before switching to Expedia four years later. However, it is unclear how many seniors actually use the AARP website versus purchasing directly with suppliers (some of which also offer discounts via AARP) or indirectly on an OTA.

For some non-travel organizations, travel is not just incremental, but part of their core offering. For example, big box retailer Costco, with its 119 million members, sells travel services through its Costco Travel portal. Costco acts as a travel agency and negotiates discounts direct with suppliers: Members can find vacation packages and cruises alongside cleaning products and electronics, which are all positioned as unique deals. Executive Members earn a 2% reward when booking on Costco Travel. If members use the co-branded Costco Anywhere Visa by Citi, they earn an additional 3% back on travel purchases.

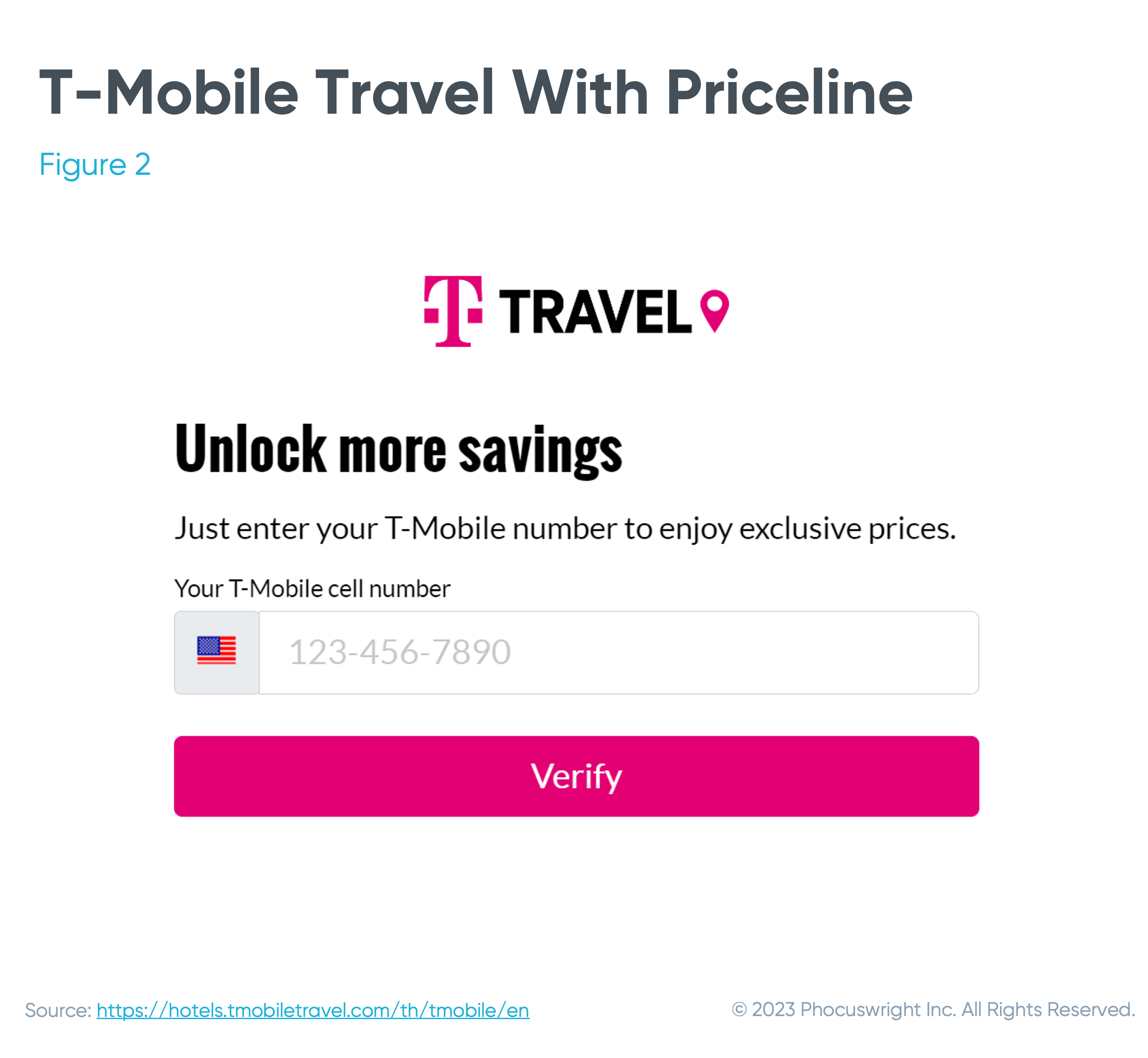

Costco wants to hit customers with travel offerings when they are in buying mode – i.e., charge card in hand. The strategy must be working: For at least the first two years after its 2016 launch, Costcotravel.com received 98% of its referral traffic from Costco.com. The website is also widely used, attracting nearly 3.7 million unique visitors in the first quarter of 2023, and ranking #14 in the Hotel and Accommodations category, just behind Choice Hotels, according to Similarweb.

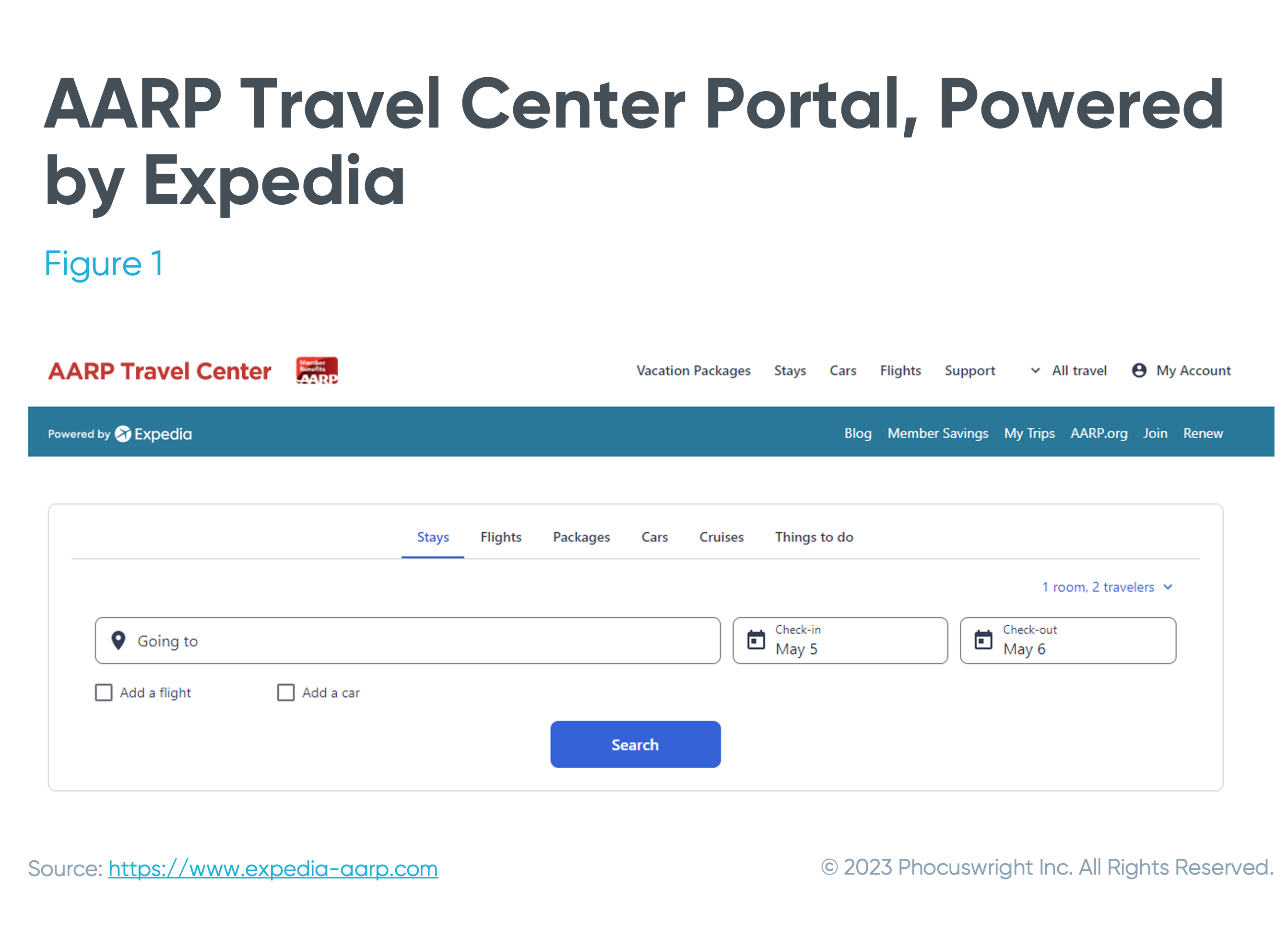

Another relatively new online offering in the non-travel category is from T-Mobile, indicating that even phone companies want to sell travel (again). In 2022, T-Mobile joined forces with Rocket Travel to launch T-Mobile TRAVEL with Priceline, offering “steep travel discounts exclusively” for T-Mobile customers, according to the company. Anyone with a T-Mobile number can get a code to unlock exclusive savings and plan their trip (see Figure 2).

T-Mobile has much less traffic than Costco Travel, but still attracts 750,000 unique monthly visitors according to Similarweb (see Figure 3).

Not every retailer has succeeded in selling travel. Walmart was a trendsetter, selling air, car and hotel on its website in the early 2000s. But it has since shut that down; travel is no longer an option on the Walmart U.S. website. However, Walmart did make another move when its Flipkart subsidiary acquired Mumbai-based OTA Cleartrip in 2021; the Middle East business was recently sold to Wego in 2022. Amazon, with its 150 million+ members, was speculated to be a big travel competitor, but that has (so far) not materialized, though it does sell travel in India via partnerships with MakeMyTrip and Indian Railways. Even Google left the scene (for now) by discontinuing Book on Google for flights and hotels.

Banking and Travel: A Marriage of Convenience

One of the most famous banking institutions with a travel program is American Express. Expedia has supported American Express Travel’s online and offline agency business for over a decade, offering travel packages and perks to cardholders and Membership Rewards members. And corporate arm Amex GBT uses Expedia’s Rapid API to power accommodations supply (Expedia sold its Egencia corporate travel business to Amex in 2021).

Most newcomers in the OTA space are financial institutions, and for good reason. They already have a captive audience of consumers who use their cards to pay for travel products. They also offer co-branded cards with airlines and hotels, but much of that loyalty goes to the supplier once a booking is made. Banks want more of the action. By offering travel bookings themselves, they can boost card usage and earn commissions at the same time.

JPMorgan Chase & Co.

The most ambitious financial institution as it relates to travel is JPMorgan Chase & Co., which plans to operate its own OTA platform in lieu of using a private-label offering. Chase already has co-branded credit card relationships with airlines including Southwest, United, Aer Lingus and British Airways, along with hotels such as IHG, Marriott, Hyatt and Disney, making travel retailing just too hard to resist. In its quest to build an end-to-end travel solution, the company made two important acquisitions: proprietary travel platform cxLoyalty in 2021, and mega leisure and corporate travel agency FROSCH in 2022. The new offering is still in development and JPMorgan Chase would not comment further except to say, “New elements of chasetravel.com are rolling out and the company is poised for a more formal launch in the back end of ‘23/early ’24.”

The financial firm makes a good case for launching an OTA. “Travel is at the center of our card business,” said Marianne Lake, JPMorgan's co-CEO of consumer and community banking, at their 2022 announcement. The company asserts that for every $4 spent on leisure travel in the U.S., $1 is spent on a Chase card, and $1 in every $3 is spent by a Chase customer. Chase would like more of that spend to not only be transacted on their cards but also purchased on the Chase platform, earning commissions of about 10%. At the time of the announcement Lake said they expected to sell $10 billion in travel in 2023 and reach $15 billion in volume by 2025, if not before. Those are big projections. (For comparison, Hopper recorded about $5 billion in gross bookings in 2022.)

Capital One

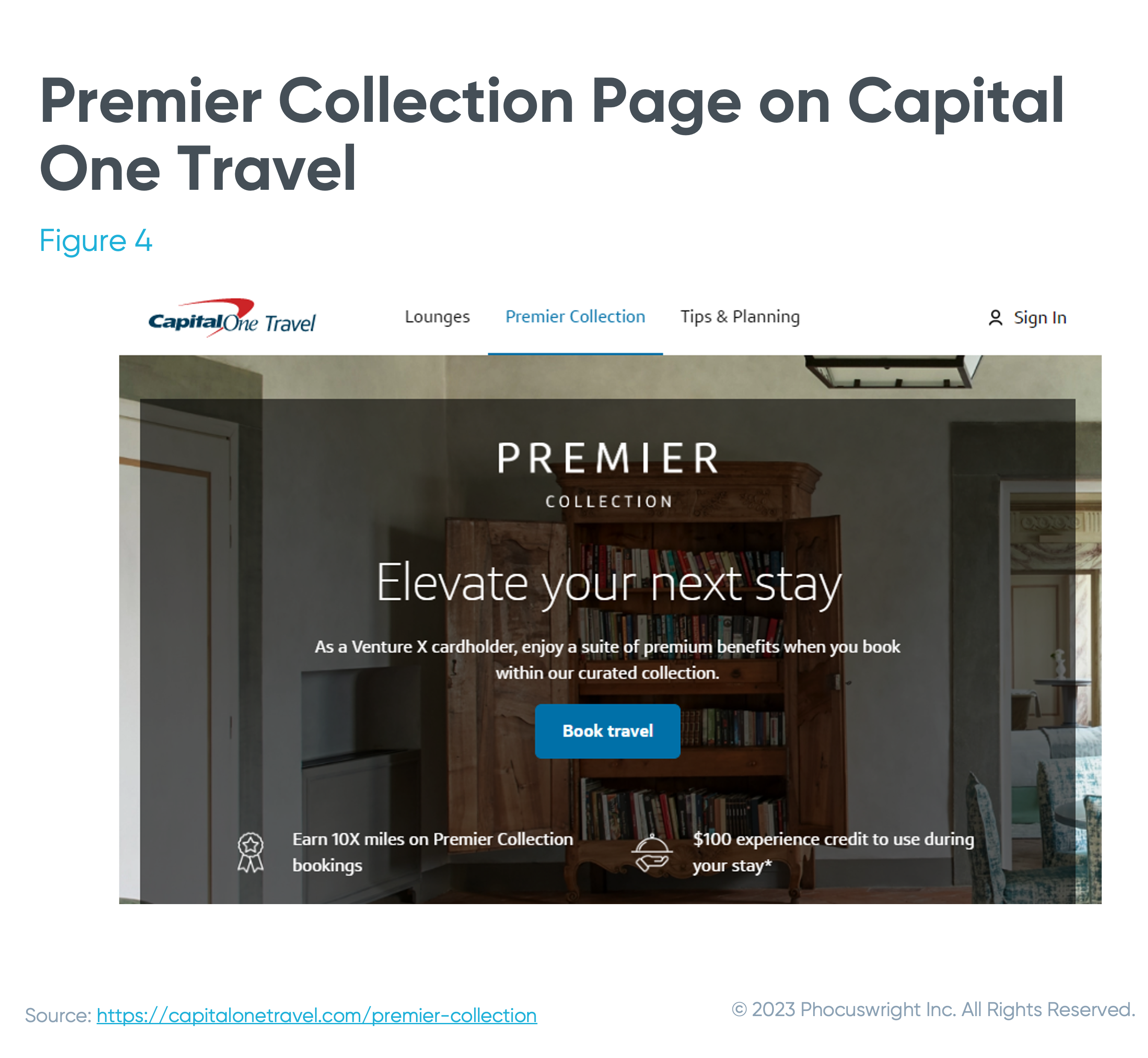

Many other financial institutions are also attracted to the prospect of engaging customers early in the travel process. Capital One entered the booking fray in September 2021 by using Hopper Cloud to power its booking platform for travel rewards customers (see Figure 4). The bank invested $96 million in a follow-on investment in Hopper in November 2022 and made Capital One Travel a showcase for the initiative.

Hopper lets partners integrate and distribute Hopper fintech and/or travel agency content as well as create white-label travel portals. Although Capital One is the only announced partner to date, more are expected to come on board in 2023. “It not about what a company’s’ core competency is,” Casey Lewis, head of Hopper Cloud, told Phocuswright. “It’s about who they are and what their customers want.” While there are many different arrangements for partners that use Hopper Cloud, the company prefers a shared revenue model so each party participates in the service’s success. Although there are few details available about the performance of Capital One Travel and other partner sites, Hopper Cloud now comprises more than 40% of the company’s revenue and is growing fast.

Citi

In March 2023 Citi officially launched Citi Travel with Booking.com, which is powered by Rocket Travel using Agoda’s technology. Citi ThankYou cardmembers can access inventory on the bank’s website or app and have the option to pay for travel with their Citi credit card, ThankYou Points, or a combination of the two; they can also earn ThankYou Points which can be redeemed in the future.

Expedia Adds More Partners

Expedia keeps adding new partners from the financial services sector, most recently announcing a joint venture with MasterCard called Travel with Rewards. Expedia also powers the travel component of RBC’s flagship loyalty program, Avion Rewards. Cardholders can access Avion’s Air Travel Redemption Schedule and redeem a fixed number of points for air bookings. In another Expedia partnership, TD Bank credit card holders can access Expedia for TD to book travel and gain rewards. In November 2022, Expedia partnered with ‘Buy Now, Pay Later’ company, Afterpay, to offer a co-branded app for travel bookings and interest-free installment payments. And \recently, Expedia announced its partnership with San Francisco-based digital finance company SoFi Technologies Inc. SoFi Travel offers members discounts and 3% cash back on bookings made with the SoFi credit card.

Other fintech offerings include U.K.-based banking app Revolut, which launched Revolut Stays in summer 2021. According to Revolut, Stays allows customers to book select Expedia and Vrbo accommodations through the Revolut app. Stays customers can book trips and receive 10% instant cash back. And U.S. Bancorp acquired travel and expense platform TravelBank in November 2021. The merged company provides integrated expense management, travel bookings and digital payments solutions.

The Long Tail Gets Longer

Considering the proliferation of plug-and-play platforms, white-label offerings and API integrations (see Figure 5 examples), it’s no wonder that becoming an OTA is hard to resist. The advantages for banks, rewards programs, retailers and other membership organizations to offer additional value with little up-front cost are obvious. And more offerings are anticipated to launch in the coming months and years. But just how big can these new offerings get? Will their quest to create pockets of loyalty work in travel, where consumers are well-trained to go to existing OTA and supplier brands? Answering these questions is complicated because each player has unique goals that can’t be measured by existing standards of volume and profits, but rather by overall customer satisfaction.

Examples of Popular "White Label" Travel Offerings

Figure 5

|

Company |

Offering(s) |

Details |

Selected Non-Travel Partners |

|---|---|---|---|

|

Expedia |

White label template or EPS Rapid (API) |

Booking template with access to Expedia.com inventory and functionality, loyalty integration, and B2B tools from Partner Solutions. API product provides customized, end-to-end hotel offerings, from shopping to booking to payment. |

MasterCard, AARP, American Express, JPMorgan Chase, Scene+, TD Bank, Royal Bank of Canada (RBC), Revolut, AfterPay, SoFi |

|

Booking.com |

Booking.com, Rocket Travel by Agoda |

API and a suite of co-branded and hybrid white label solutions by Booking.com and Rocket Travel by Agoda. |

T-Mobile, Citi, Venmo, Apple |

|

Hopper |

Hopper Cloud |

Suite of fintech and travel agency products provides white label access to Hopper’s inventory of flights, hotels, rental cars, and financial offerings. |

Capital One, Uber |

Finally, how are new launches going to impact the marketplace? Undoubtedly new websites and apps will further fragment the OTA landscape. But since so many of them use an existing OTA platform, they might merely be siphoning business from one booking engine to another instead of creating new opportunities. It is therefore unlikely that these bank and rewards-based offerings will make a huge splash individually, especially since OTAs and suppliers have their own competing loyalty programs.

But they could, in aggregate, generate a ripple effect as travelers choose to shop, pay and redeem rewards all in one place. Just don’t expect anyone to replace the mega-OTAs anytime soon; if anything, these developments will only make them bigger.

This article is part of a content series that explores some of the most impactful innovation and technology-driven trends that will influence the travel industry in 2023 and beyond.

Below is a link to each full trend analysis.

- The Future of Social Media, Influencers and Social Commerce in Travel

- Web3 Is Proving Itself in Travel

- Green Travel Innovation Now (Yes, Now!)

- No Travel Experience Necessary: More Outsiders Enter the OTA Market

- Generative AI: Transforming the Travel Cycle

- Real-time Revolution in Hotel Operations

- eVTOLs in Travel: Viable Addition or Flights of Fancy?

- Super Apps’ Secret Sauce

Watch the online event that covered each trend, presented by Phocuswright analysts: